Chris Forrester — SES cancelling two Intelsat satellites (IS-41 and IS-44) generated plenty of headlines since the announcement was made during the operator’s quarterly results statement on May 12. This news, plus a similar cancellation made by Eutelsat of its Eutelsat Americas craft earlier this year has brought into focus the question of the importance of geostationary satellites and whether they have a future..

Without doubt GEO craft are perfect for the ‘one-to-many’ roles that DTH/DBS typically demand. Indeed, the likes of SES, Eutelsat, Telesat and local players such as DirecTV and EchoStar have banked billions of dollars from their ‘cash cow’ investments in orbital Geo satellites. SES built its lucrative dominant position because of DTH over Europe. In fact, this past week it announced that Germany’s ARD public broadcaster has renewed its satellite delivery contract to 2039.

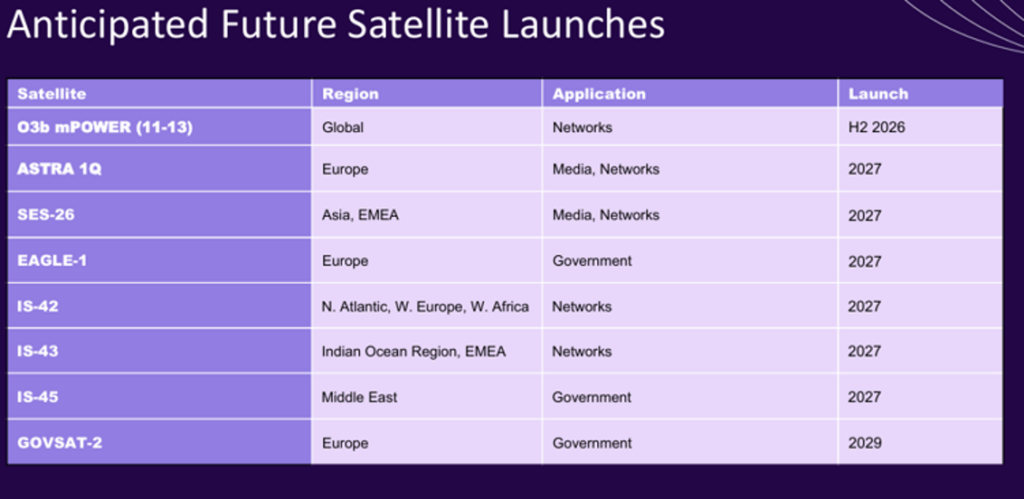

The Eutelsat cancellation of its ‘flexible’ Americas craft means it now has no geostationary orders in its manifest. This is not the case with SES which still has five media or government-related craft on order (Astra 1Q, SES-26, IS-42, IS-43 and IS-45). In other words, the SES decision is firmly one of rationalisation and consolidation of overlapping coverage now that Intelsat is fully absorbed.

SES did not specify the full rationale behind the cancellations other than that the satellites were not now needed and had not met its investment return expectations although SES is also considered mission extension options for certain existing craft in the Intelsat fleet.

CE Adel Al-Saleh stated: “Following the Intelsat acquisition, SES is optimizing across a larger, more resilient satellite fleet and reducing unnecessary duplication. As part of this normalization, SES is cancelling two software defined satellite orders while retaining ample flexibility through four others and leveraging existing fleet capacity to ensure seamless, uninterrupted service for customers.”

Cancelling the pair certainly helps SES CapEx commitments even if there are cancellation penalties to be paid. SES said that prior to the acquisition of Intelsat the combined 95-satellite fleet would need consolidating. These cancellations are part of that rationalisation. SES stressed and reiterated its FY2026 CapEx outlook, which includes the cancelation of the satellites.

“We have taken some pretty hard decisions on which satellites we need and which can use extension vehicles so we did not need to procure” replacements, SES CFO Lisa Pataki added during the earnings call with analysts.

For North America and the US in particular SES is keeping its powder dry until the FCC makes its decision later this year on what it intends to do with its C-band Mk-2 auction. While there were no material updates on C-band during the results announcement, an FCC ruling on the next stage of C-band is expected in Q2/2026. However, CEO Adel Al-Saleh told analysts that the SES Ku Plus solution for replacing existing satellite feeds was being welcomed by US clients. This will mean new geostationary satellites although the FCC’s auction will be expected to fund their build and launch costs.

Meanwhile, Geo-based media revenues continue to decline. Al-Saleh spelled out the realities, saying: “Our Media business (34% of total revenues) continues to have a strong cash-generative profile and despite structural headwinds the business has secured close to €100 million in long-term renewals and new business in the first quarter,” he stated. Media revenues of €285 million was up +42.9% y-o-y, benefiting from fully consolidating Intelsat from 17 July 2025.

It is much the same elsewhere in the Geo-sphere. Telesat’s Q1 numbers (released on May 5) admitted “ongoing revenue pressures” and revealed a 26% fall (year-on-year) fall in its Geo-related revenue to (Canadian) $86 million. CEO Dan Goldberg said: “The revenue decline was driven primarily by non-renewals of certain broadcast contracts in 2025 and, to a lesser extent, reductions in services for fixed broadband customers.”

Eutelsat’s numbers were released on May 12 and the operator said it continues to suffer a steady decline in Video segment revenues which were down 13.3% (y-o-y) for Q3 at €128 million (€151.7m last year). Eutelsat explained the fall, saying: “This reflects the impact of sanctions on Russian channels imposed at the beginning of the year, (c. €16 million per annum) as well as the termination of capacity contracts on the Express AT1 and AT2 satellites (low single-digit million impact in FY 2025-26 starting from March 2026), in addition to the underlying decline of this mature business.”

The underlying decline of these mature video contracts is a phrase that can be uttered by almost anyone in the DTH/DBS business. DirecTV and EchoStar have lost millions of subscribers who have turned to streaming for their entertainment.

The shift to LEO and MEO by operators is clearly dramatic, and that’s where the future money is. SES is building on its mPOWER fleet. Eutelsat is doing well with its OneWeb fleet. Both parties are backing the European IRIS2 planned mega-constellation of satellites. Europe will make a decision on this scheme during its ‘Rendezvous-1’ consultation. This decision was initially expected by April 30, and now the word on the street is that a decision will come in the next few weeks.

SES told analysts that its new MeoSphere plans for orbiting at 8000 kms and is firmly “our next-generation network”. It will support multiple missions with flexible space segment, and compact terminals (50cm x 50cm) and be 5G compatible and ‘plug and play’ operationally and come into use by the end of this decade. The satellites come from smaller manufacturer K2.

It is the same for Telesat which is putting a fortune into its Lightspeed LEO constellation likely to come into use by early 2028.

EchoStar has been more or less financially rescued by the now FCC approved sale of frequencies to AT&T and SpaceX.

Eutelsat is buying around 400 new OneWeb satellites as part of its fleet replacement mission.

SES is also backing Lynk Global and Omnispace coming together and will then invest in the combined pair for their LEO scheme.

And any one of these players can buy new Geo-based craft from K2 as well as SWISSto12 and its ‘Hummingsat’ smaller satellites. SES, for example, already has an order in place with SWISSto12 for a replacement satellite for the damaged Intelsat IS-45 craft and due for delivery in 2027. Viasat also has three Inmarsat 8 satellites on order for delivery in 2028 from SWISSto12. All three Viasat/Inmarsat craft will be delivered on the same rocket and then use their on-board electric orbit raising thrusters to reach their targeted positions.

In other words, Geo is far from dead, but times have changed. The savvy players are investing in LEO or MEO fleets, as well as sweating their existing orbital assets. And nobody is going to ignore long-standing contracts from Geo-based broadcasters with millions of viewers depending on satellite signals.