Professor Tim Farrar of TMF Associates has released a comprehensive new analysis detailing the consumer business prospects for Starlink. Published on June 5, 2026, the report arrives at a critical juncture for the commercial space sector as the industry braces for the highly anticipated SpaceX initial public offering.

The deep dive provides the first detailed geographical breakdown of Starlink’s global customer distribution, utilizing meticulous weekly monitoring of active satellite terminals to project future subscriber bases and revenues across various countries and regions.

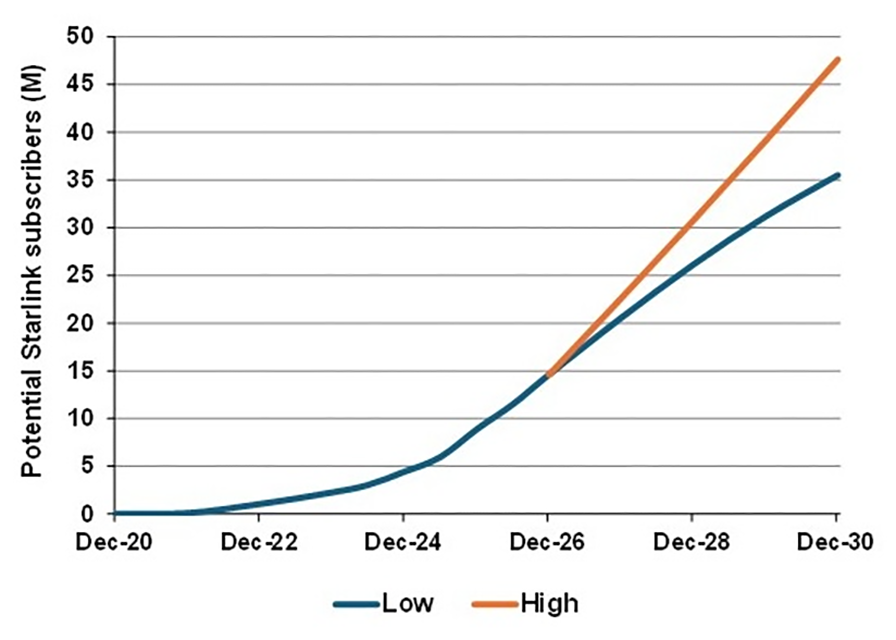

Historic Growth and Future Trajectory

The historical data presented in the report summary illustrates a staggering pace of customer acquisition. Starlink’s global subscriber count has experienced explosive year-over-year growth, climbing from 2.3 million in 2023 to 4.4 million in 2024. The network then doubled again to reach 8.9 million users in 2025. As of the end of the first quarter in March 2026, the active subscriber base has surged to 10.3 million users.

Looking forward, the report’s headline forecast suggests that this momentum is far from slowing down. Farrar outlines a “Bull case” scenario in which Starlink could capture more than 45 million subscribers by the year 2030. Even the more pessimistic “Bear case” projection estimates that the satellite internet provider will secure a massive customer count exceeding 35 million by the end of the decade. Analysts note that Starlink may even target a doubling of its subscriber base to reach 18 million global users by the end of 2026.

Navigating Terrestrial Competition and Capacity Limits

Despite the bullish projections, the report carefully outlines the potential limitations to Starlink’s future growth. A primary challenge will be how successfully the satellite operator can compete against established terrestrial alternatives in densely populated or highly developed countries. To maintain its rapid cadence of growth, particularly in mature markets like the United States, Starlink will need to increasingly capture market share from traditional telecommunications and cable internet providers, potentially utilizing aggressive pricing strategies as a lever to attract new consumer demographics.

Furthermore, the physical limitations of orbital infrastructure remain a crucial factor. Starlink currently possesses a network capacity capable of supporting approximately 20 million broadband subscribers. Scaling beyond this threshold to reach the 40 million mark will necessitate the continued mass deployment of V2 Mini satellites utilizing the Falcon 9 launch vehicle, alongside the successful introduction of next-generation hardware architectures.

Assessing the Threat from Amazon LEO

The analysis also dedicates significant attention to the looming competitive threat posed by Amazon’s Low Earth Orbit constellation. By comparing the underlying technologies and deployment timelines of both networks, the report assesses whether there is any realistic prospect of Amazon making significant inroads into Starlink’s market dominance in the coming years.

While Amazon possesses a formidable retail presence and vast financial resources, its initial constellation of 700 satellites is projected to only support around 1.5 million broadband subscribers. This stark contrast in immediate network capacity suggests that Starlink will likely maintain a comfortable lead in subscriber acquisition, forcing emerging competitors to aggressively scale their launch cadences and orbital infrastructure if they hope to capture a meaningful share of the booming satellite broadband market.