Whoever controls the home menu screen controls content discovery, user data collection, and advertising inventory placement.

The strategic value of television has shifted from hardware manufacturing margins to the control of the home screen user interface. Because hardware margins on television sets have dropped close to zero, the TV OS has become the most valuable real estate in digital advertising.

The competitive landscape features massive consolidation and strategic entries:

- Media Companies Owning the Gateway: Fox executed a massive $22 billion acquisition of Roku. This vertical integration marries Fox’s premium live sports and news content infrastructure directly with Roku’s 100-million-household OS deployment, allowing Fox to bypass third-party gatekeepers and target programmatic advertising based on granular Roku user data.

- Retail Networks Entering the Living Room: Walmart finalized its $2.3 billion acquisition of smart TV manufacturer Vizio, withdrawing the brand from external retailers to position it as an exclusive private label. Coupled with its $1.4 billion purchase of streaming advertising technology firm Vibe.co, Walmart is converting Vizio’s software platform into a direct extensions of its Retail Media Network (RMN), blending home screen viewing data with real-world consumer shopping habits.

- Pure Ad-Tech Disruptions: Advertising technology firms like The Desk have built independent operating systems (such as Ventura) to compete directly against hardware manufacturers without owning any native content libraries, offering publishers an unbiased alternative to tech-walled gardens.

Market Concentration and the “Gatekeeper” Dynamic

According to recent analytics data, the connected television operating system environment is highly concentrated among a select tier of dominant platforms that dictate market access:

| Operating System Platform | Approximate U.S. Connected TV Usage Share | Strategic Asset Focus |

| Roku OS | 28% | Independent Ad Inventory & Media Network (Fox) |

| Samsung Tizen OS | 23% | Global Hardware Volume & First-Party AVOD (Samsung TV Plus) |

| Amazon Fire TV | 17% | E-commerce Funneling & Prime Ecosystem Integration |

| LG webOS | 10% | Global Software Licensing to Third-Party B-Brands |

Because these platforms govern the interface, they act as strict gatekeepers. If a premium streaming service or an interactive satellite application wants to be discovered by a consumer, it must negotiate revenue-sharing terms, ad-inventory allocations, and home-screen button placements with the underlying operating system provider.

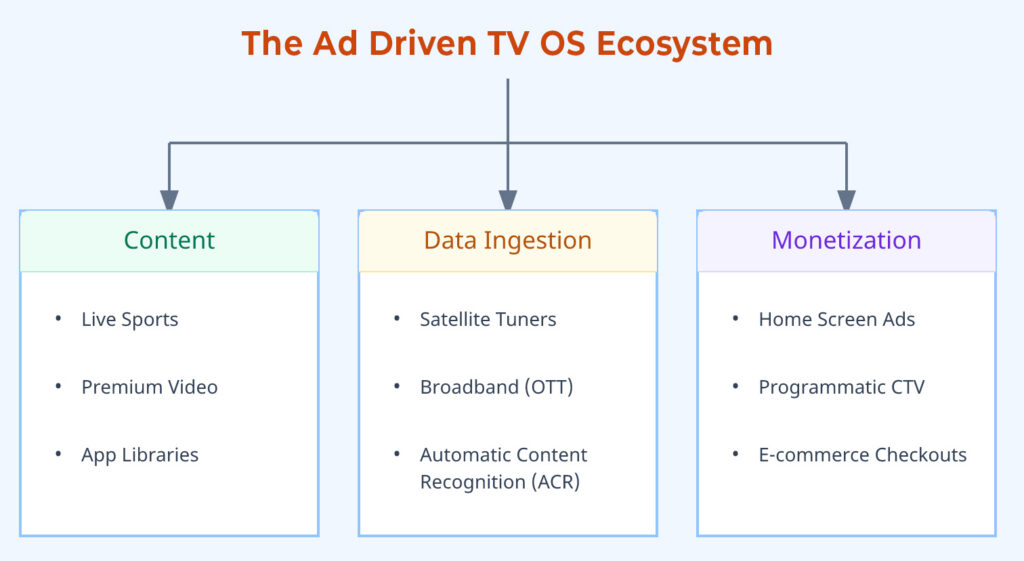

Ultimately, your television screen is no longer a simple terminal designed to receive external orbital satellite broadcasts. It is an intelligent, connected computational asset where content creation, retail commerce, and satellite-terrestrial data streams converge into a single, highly monetizable user interface.