By Evan Grey, Legal Contributor, SatNews

For decades, the satellite industry operated under a coordination framework designed to manage interference through established ITU and FCC procedures. As of today, January 8, 2026, that framework is facing a definitive stress test. The industry has entered a phase of industrial-scale deployment where sheer constellation size is shattering long-standing assumptions about orbital and spectral coexistence.

This week’s news exposes a “Sovereign-Commercial Nexus”—a strategic realignment where states are intervening directly to preserve orbital autonomy. In Europe, officials are accelerating “Irisization,” executing a coordinated pivot to reclaim their digital sky. Simultaneously, a regulatory trench war has erupted in Washington. Legacy operators are pressing the FCC to act as a firewall against an unprecedented expansion of private orbital power.

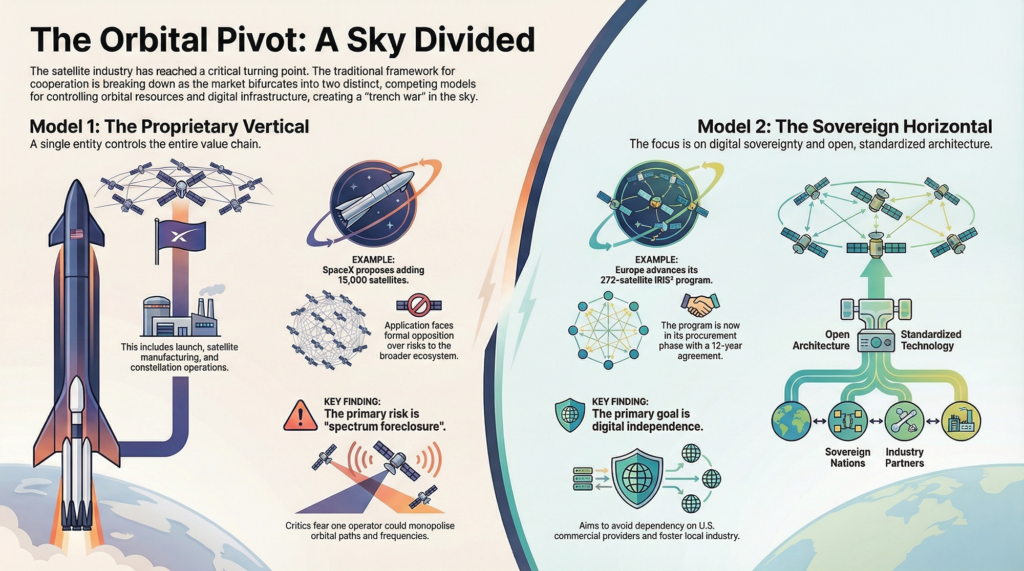

The 15,000-Satellite Intervention

The U.S. regulatory process hit an inflection point this week. On January 6 and 7, 2026, a coalition of operators, including Viasat, SES, Globalstar, and Eutelsat, filed formal petitions to deny (GN Docket No. 25-340) challenging SpaceX’s latest modification application. Accepted for review via Public Notice DA 25-1018, the filing seeks authorization to deploy an additional 15,000 satellites in a new Very Low Earth Orbit (VLEO) shell at approximately 330 kilometers.

SpaceX pitches the application as Supplemental Coverage from Space (SCS), but the opposition, coordinated largely through the Mobile Satellite Services Association (MSSA), sees it as spectrum foreclosure. In their pleadings, Viasat and its partners argue that allowing a single operator to occupy such a dense, low-altitude regime invites interference and creates severe constraints for the broader ecosystem. Blue Origin weighed in with its own comments, warning that sustained operations at a 330 km shell could physically limit the ability of other launch providers to conduct missions safely.

Brussels and the SpaceRISE Pivot

Washington is debating spectrum and process; Brussels is deploying capital. On January 5, the SpaceRISE consortium, comprising Eutelsat, SES, and Hispasat, pushed Europe’s IRIS² program into its procurement phase. This follows the signing of a landmark 12-year concession agreement and the issuance of RFPs for the system’s 272-satellite LEO segment.

IRIS² is structured as a multi-orbit architecture spanning LEO, MEO, and GEO, explicitly designed to secure European digital sovereignty. The program mandates that at least 30 percent of project value be subcontracted to SMEs. This policy aims to cultivate a parallel industrial ecosystem, avoiding the deep vertical integration characteristic of the U.S. market. With core engineering roles involving Thales Alenia Space and bids centering on Airbus Defence and Space, Europe is moving to insulate critical infrastructure from dependence on U.S. commercial super-primes.

The Bifurcation Point

The industry has reached a true bifurcation point. Capital flows, technical standards, and strategic intent are splitting the market into two distinct models:

- The Proprietary Vertical: Exemplified by the “Musk Stack,” where a single entity controls launch, spacecraft manufacturing, constellation operations, and the software-defined intelligence layer.

- The Standardized Horizontal: Anchored in 3GPP Release 19 and gaining momentum through satellite-native consumer hardware. This shift was on display at CES 2026 with the debut of the Infinix Note 60 series. While its current 4 kbps throughput remains a limitation, the device’s always-on global voice and SMS capability signals a move beyond emergency-only satellite access toward true mass-market integration.

The era of the unaligned satellite operator is over. As IRIS² manufacturing timelines accelerate and the FCC weighs the implications of a 15,000-satellite expansion, the sky is no longer merely a medium for data transmission. It has become a central arena of global industrial policy. The Orbital Pivot is underway, and the industry must now choose between the efficiency of proprietary dominance and the resilience of sovereign systems.

About the Author:

Evan Grey is a legal contributor for SatNews. A lawyer with a focus on regulatory policy and international relations, he specializes in the evolving geopolitical and industrial frameworks of the global space sector.