SatNews Editorial Analysis, Edited by Simon Payne, Abbey White

Executive Brief

- The Rebrand & Rollout: Formerly Project Kuiper, the newly christened Amazon Leo launches in Q1 2026 with a three-tier hardware strategy targeting the US, UK, and Germany first.

- The Scale Engine: While Amazon will fight for consumers with its Nano and Pro terminals, this volume play primarily serves to drive down chip costs for its true endgame: the industrial-grade Ultra backhaul network.

- Physics Over Hype: Unlike AST SpaceMobile, which uses massive satellites to overcome phone limitations, Amazon accepts the physics of small antennas, prioritizing high-speed fixed terminals over the direct-to-device novelty.

Late to the Market, Early to the Model

If you listen to the Silicon Valley echo chamber, Amazon Leo is already dead on arrival. The critique is seductive in its simplicity: SpaceX has 6,000+ satellites and 4 million subscribers. AST SpaceMobile just launched the largest commercial array in history to turn every smartphone into a satellite phone. Meanwhile, Amazon is just now ramping up to meet a critical FCC deadline in July 2026.

The conclusion seems obvious: Amazon missed the consumer revolution. But this hot take misses the nuance of Amazon’s new three-tier strategy. This isn’t a play for consumer mindshare. It’s a bid to control the infrastructure layer of space.

The Trojan Horse: Consumer Broadband

Amazon is coming for the consumer, but they are doing it with a ruthless focus on hardware segmentation. In late 2025, they revealed the lineup that will power their Q1 2026 launch in five key markets (US, UK, Germany, France, Canada):

- Leo Nano: A 7-inch portable square delivering 100 Mbps. Small, cheap, and designed to undercut Starlink’s Mini.

- Leo Pro: The standard 11-inch residential unit pushing 400 Mbps.

- Leo Ultra: A massive 19×30-inch enterprise terminal capable of 1 Gbps.

Here is the strategic twist: The Nano and Pro consumer terminals are quite possibly the scale engine. The secret sauce inside every box is the proprietary Prometheus chip.

For those outside the silicon trade, it’s hard to overstate what Amazon’s Prometheus chip represents within the emerging satellite broadband ecosystem. Amazon’s custom silicon unifies functions typically handled by multiple discrete components (advanced modem processing, phased array control, and network routing) into a single integrated design. By deploying this same chip across millions of Nano and Pro consumer units, Amazon can leverage manufacturing scale to push Prometheus down the cost curve over time. While Amazon has not disclosed internal unit economics, this volume-driven approach to custom silicon materially improves the feasibility of higher-performance, industrial-grade Ultra terminals, hardware that would be far more expensive to produce at low volumes. In effect, consumer broadband becomes the mechanism that enables Amazon’s backhaul-first strategy to compete on price while preserving the economics of its B2B focus.

The Frenemy Dilemma: Why Amazon is Unique

While Starlink also offers business tiers, its ambition to become a global consumer telco makes it a threat to carriers. For a company like Verizon or AT&T, Starlink is a frenemy: a partner today, a predator tomorrow.

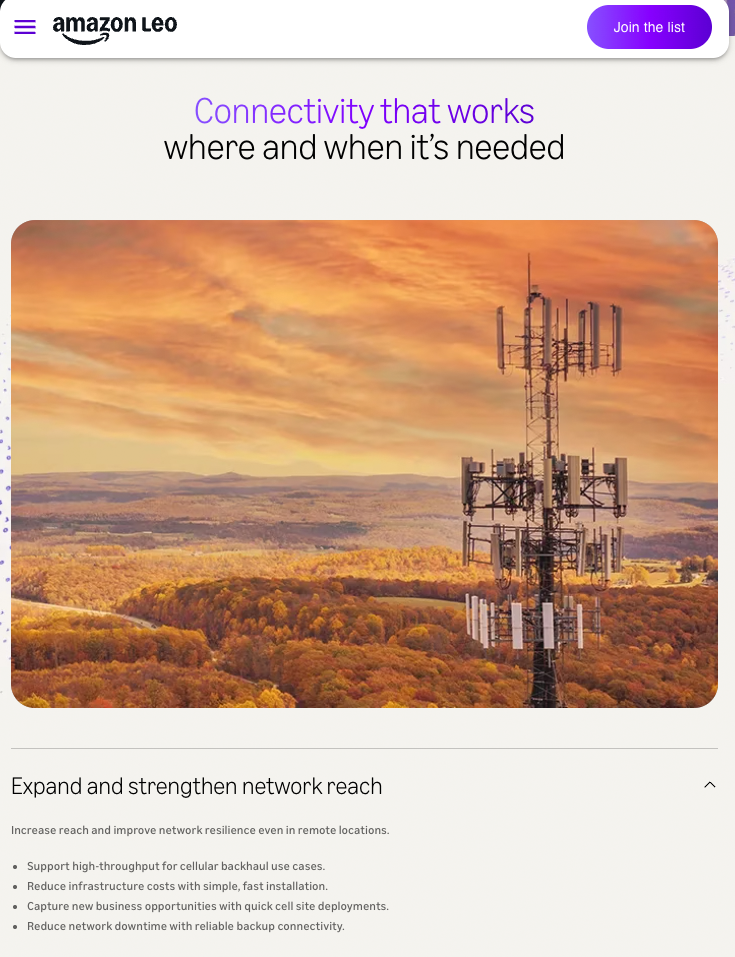

Amazon’s unique play is neutrality. The Leo Ultra terminal allows Amazon to act as a flying fiber provider. They sell the pipe to the telco, who then distributes it to the end user via a cell tower. Amazon explicitly signaled this B2B loyalty in a regulatory submission to the Australian Communications and Media Authority (ACMA), arguing that relying on direct-to-device (D2D) for universal service was “premature“. This was a dog-whistle to telcos: We aren’t trying to bypass you like Starlink; we are here to support you.

The Physics of an Unbent Pipe

This backhaul first strategy is grounded in the Shannon-Hartley theorem, which creates a brutal trade-off between convenience (D2D) and capacity (Backhaul).

- The Whisper (AST & Starlink): AST SpaceMobile is betting the company on overcoming this limit with BlueBird 6, a satellite with a phased array spanning nearly 2,400 square feet. It is an engineering marvel designed to squeeze 120 Mbps out of a weak smartphone signal. However, that bandwidth is shared across an entire cell.

- The Shout (Amazon Ultra): By using the high-gain Leo Ultra dish, Amazon increases the signal strength by orders of magnitude. This allows them to push 1 Gbps to a specific location, which a local tower can then distribute as standard 5G.

While AST chases the magic trick of connecting your phone anywhere, Amazon is betting that users actually want the high-speed video and app performance that only a powered tower (fed by Leo) can provide.

Building the Backbone, Under the Clock

The strategy is sound, but the execution remains perilous. Amazon is currently locked in a deployment surge. They have roughly 150 satellites in orbit today and must launch half their constellation by July 2026 to keep their license.

If they execute, the industry will see a bifurcation: Starlink and AST fighting for the consumer’s pocket with direct connections, while Amazon Leo quietly becomes the invisible backbone of the global economy, moving data for the Fortune 500 and telcos alike.

Twenty years ago, Wall Street laughed at an online bookstore trying to rent out its excess server capacity. They called it AWS. Today, Amazon isn’t trying to win the space race for the headlines; they are trying to win the backend. And if history is any guide, the most profitable place to be isn’t the star of the show, it’s the stage manager.